Note: Note: This content is for informational purposes only and not investment advice. The views expressed are personal opinions and may be incomplete or incorrect. Any references to asset allocation or investments are illustrative, not recommendations. Markets and exchange rates are volatile, and investing involves risk. Do your own research or consult a qualified advisor. The author is not responsible for any losses arising from this content.

As the world and the Indian economy struggle amidst the U.S.-Israel war on Iran, most Indians who hold financial assets are seeing their value decline. The Indian Rupee is also depreciating, which is putting further strain on real returns.

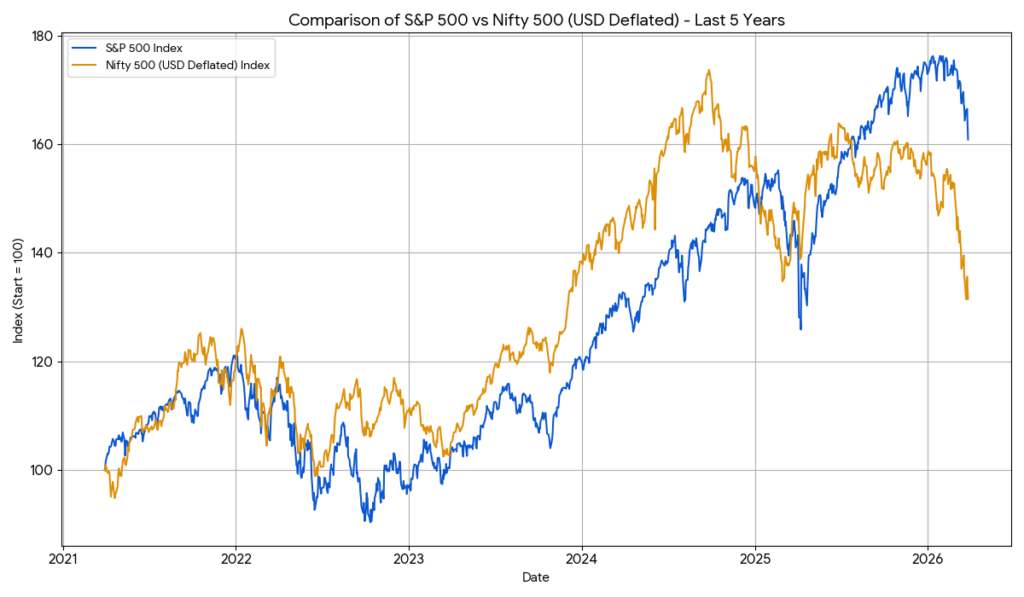

Comparing the NIFTY 500 and S&P 500 indices shows this clearly. After adjusting the NIFTY 500 for depreciation of the Indian Rupee, the return is just 31.48% over the last five years, as opposed to 60.89% for the S&P 500.

In fact, the compound annual growth rate of the NIFTY 500, adjusted for depreciation, is a mere 5.64%, just slightly above U.S. Treasuries. The difference is that U.S. Treasuries are risk-free in nominal terms, while Indian equities are highly risky.

This is why I believe Indians should hold foreign currency assets as a significant part of their portfolio. Unfortunately, many Indians tend to hold commodities or their equivalents to hedge against inflation and depreciation. The issue is that commodities like gold are not risk-free, they are highly volatile and do not always behave the way most people expect them to. For example, when the U.S. and Israel attacked Iran, gold prices dropped slightly from $5,300/oz to $4,488/oz as of 30th March 2026.

Sovereign government bonds, meanwhile, are risk-free. In fact, financial markets use the risk-free rates provided by these bonds to price their own assets, since any risk-adjusted return below the risk-free rate is not worth it for most investors.

Indians should therefore dedicate a portion of their portfolio to holding first-world sovereign bonds and other foreign assets denominated in dollars, euros, pounds, etc., to hedge against depreciation.

Some people might say that holding foreign assets is “anti-national” or similar. This is clearly wrong. If you are an Indian worker, you are paid in rupees, all your debts are in rupees, you pay your taxes in rupees, everything you buy is in rupees, and you contribute to aggregate demand. The Indian rupee is already your default exposure. Holding foreign currency assets acts as a structural hedge.

Holding foreign financial assets makes people more resilient to external shocks. It provides gains precisely when your local assets are losing value. It is more stable, and arguably more “patriotic,” not to rely entirely on a single currency’s value.

As for those who say buying foreign assets diverts funds away from local companies, this is also incorrect. Real capital formation does not primarily happen in secondary markets, which is what you participate in when you buy shares. Firms invest based on expected demand and profitability. They borrow from banks, which create new money through lending, and invest as needed if there is profit to be made.

That said, this does not mean all your financial assets should be foreign. A significant portion can be, but not 100%. Maintaining some local currency assets that are easy to liquidate without currency risk is also important.

In events of external stress, these same foreign assets can act as an automatic stabilizer for the Indian economy as a whole. You can sell part of your foreign assets and convert them into local currency assets. Doing so helps stabilize the exchange rate as well. In fact, this is one of the key mechanisms through which the currencies of richer countries remain stable during external shocks.

The Government of India allows Indians to send up to $250,000 a year under the Liberalized Remittance Scheme, even for foreign equity and debt purchases. There is nothing illegal or unpatriotic about using this to buy foreign currency assets, just be aware that you have to report which foreign assets you own under Schedule FA (and others) in your Income Tax Return.

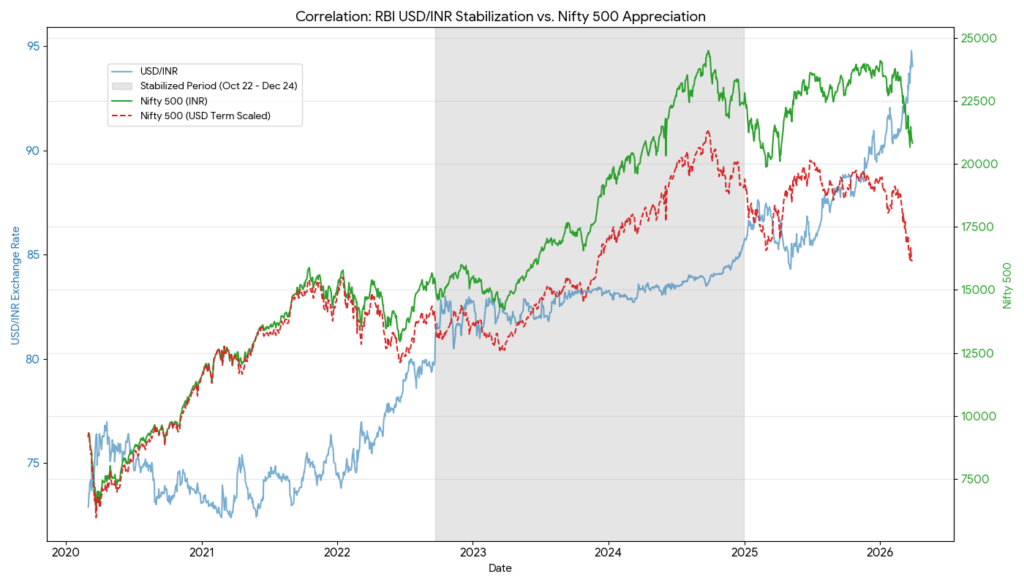

How India’s “stabilized arrangement” of its currency led to a massive boom in share prices and why it wasn’t sustainable.

I was not very supportive of the Reserve Bank of India’s rupee exchange rate policy between October 2022 and around December 2024. During this period, the RBI kept the USD/INR exchange rate stabilized around INR 82 per USD. The total movement of the currency during this entire two-year period was just 5.5%, a mere 2.5% annual depreciation, very low for the Indian rupee.

This was done mainly by drawing upon foreign currency reserves held by the RBI. Given that depreciation expectations were well anchored due to how global flows were at the time, this could be sustained without drawing down the entire stock of foreign currency reserves held by the RBI. Why? Because the stabilization itself brought in foreign capital, which led to appreciation pressure on the exchange rate, which meant pressure on reserves was reduced. In fact, despite such stabilization policies, India’s foreign currency reserves mostly grew during this period due to these inflows.

With currency risk largely gone, the equity risk premium for India went down quite a lot, and the NIFTY saw a massive sustained rally during this period. However, when the RBI was forced to abandon its currency stabilization policies around December 2024 due to Trump’s policy expectations slowing down capital inflows and putting pressure on foreign exchange reserves, the equity risk premium increased significantly. This further slowed inflows and increased outflows. The rupee has depreciated around 10% so far since the end of the stabilized arrangement period.

The entire episode showed that trying to stabilize the exchange rate can create conditions that lead to instability, given that the private sector seeks to maximize profits. As Hyman Minsky said, “stability is destabilizing.” While the NIFTY 500 had a CAGR of nearly +17.8% during the stabilized arrangement period, the period between December 2025 and the present has seen the CAGR slip to -13.8%.

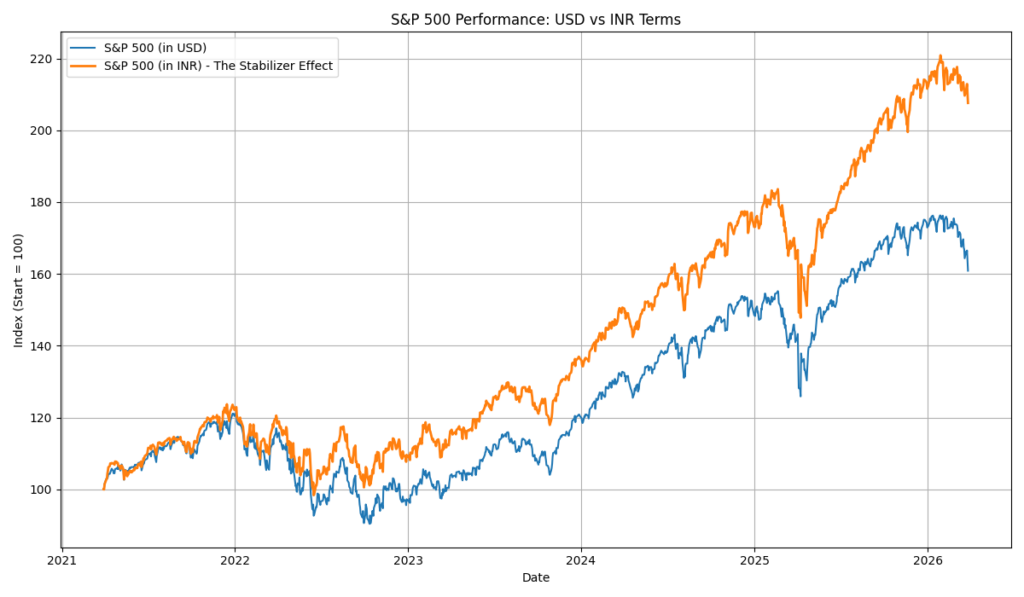

By holding the rupee stable, the RBI effectively lowered the cost of holding Indian equities for two years.

This promoted “yield chasing” behavior, especially among foreign investors, who could ignore exchange rate risk. When the exchange rate anchor was removed, much of the unhedged capital flowed back to the U.S. and other developed markets, putting more downward pressure on equity prices than would likely have occurred had the exchange rate not been stabilized.

Conclusion:

1. While Indian share markets appear sharp in local currency terms over the last five years, the USD-deflated CAGR is a mere 5.64%, barely above risk-free U.S. Treasuries.

2. For an Indian worker, the rupee is not just an asset, it is what all your liabilities are denominated in. You are already long on rupees simply by living in India and working for rupees. Holding foreign currency assets acts as a structural hedge.

3. Commodities are not low-risk hedges against uncertainty, they are vulnerable to speculation, unlike sovereign currency bonds.

4. Indians should utilize the Liberalized Remittance Scheme (LRS) provided by the Government and allocate a significant portion of their portfolio, for example 20%, into foreign currency assets. Not just dollars, but also euros, pounds, yen, etc.

That’s all.