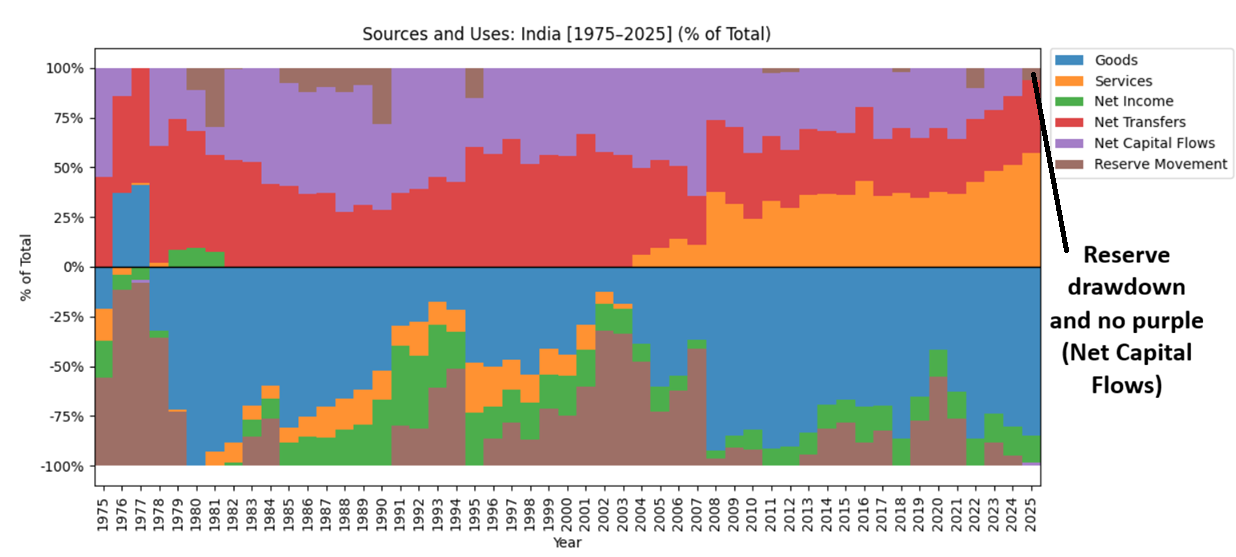

Interesting things are happening with India’s balance of payments components. For the first time since 1977, India’s net capital flows have turned negative. This means India’s entire current account deficit was financed by a drawdown of foreign exchange reserves.

India drew down approximately $22 billion worth of foreign exchange reserves to finance not only its current account deficit of roughly $16.5 billion, but also a capital/financial account deficit of nearly $5.5 billion.

This is unprecedented. India has never had a year since liberalization where net capital flows were negative, not even in 2008 or 2022. This means that, on net, the only two components (excluding reserves) financing India’s current account deficit were net transfers (remittances) and services exports, instead of the usual three positive components: net transfers, services exports, and net capital flows.

{.alignnone}

What does all of this mean? Given that the Indian rupee is floating, there is no immediate balance of payments crisis that the Indian government will face. However, the exchange rate of the rupee will continue to be under pressure.

Given the Iran war related shock, it is highly unlikely that this year will be any different. Indian equity prices have taken a heavy beating. As of 23rd April 2026, they are down 0.64% over one year.

It also implies that RBI drawing down reserves is effectively subsidizing a cheap exit for foreign ‘investors’. This is unfortunate and suggests that forex reserves should be deployed in a more targeted manner, such as providing direct lines to public sector enterprises, as I have suggested in my previous blogs.

If RBI didn’t draw down it’s reserves, it is likely that India would’ve seen it’s goods deficit compress via depreciation, so that balances balance.

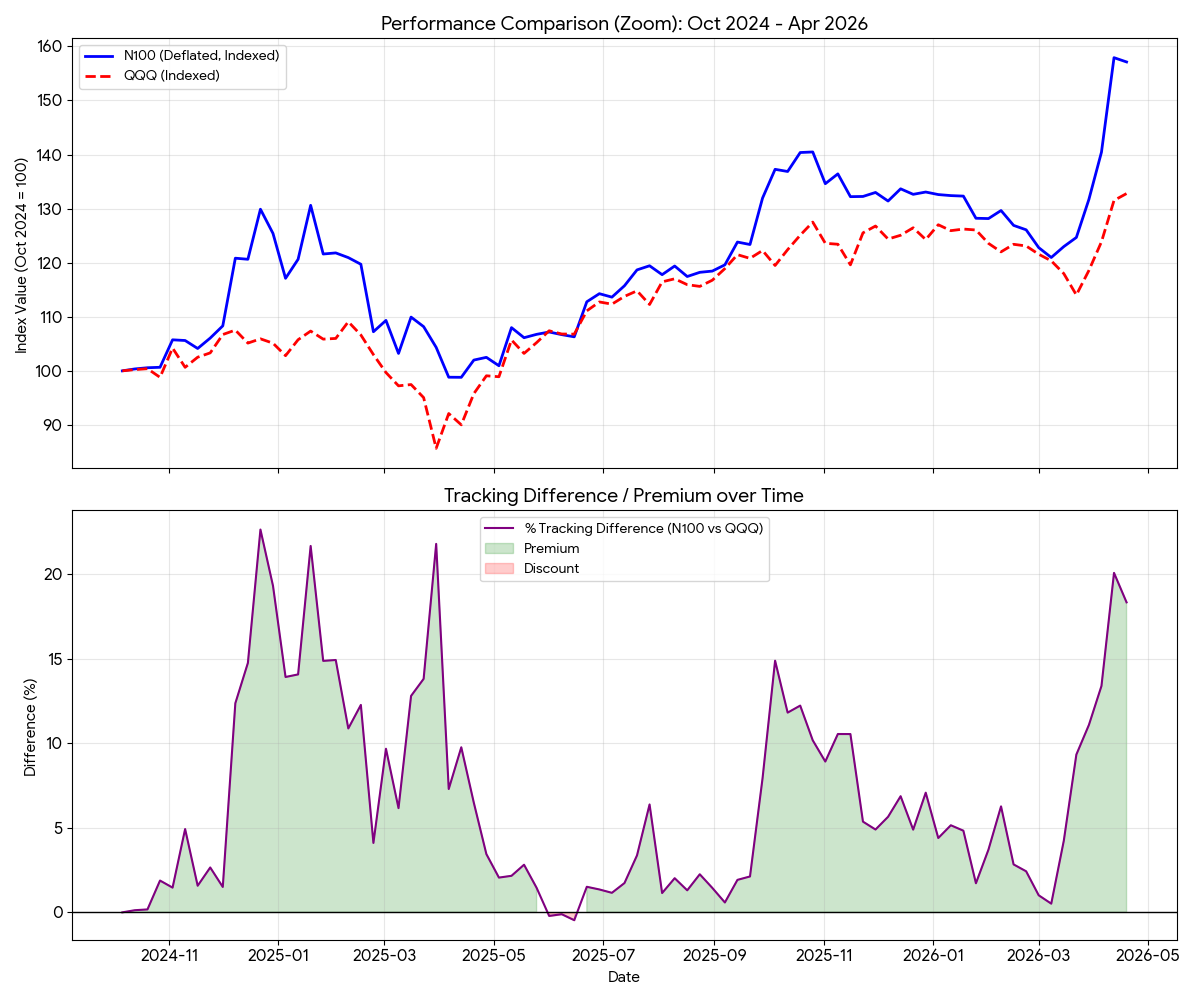

Another indicator of how much the Indian rupee is under pressure is the premium at which U.S. focused ETFs like MON100 are trading in India. These are essentially Indian exchange traded funds (ETFs) that invest in U.S. ETFs and issue their own units denominated in rupees. Since SEBI places caps on how many units of these rupee denominated ETFs can be created, the premium or discount at which they trade relative to their actual NAV becomes an important indicator of Indian investors’ desire to diversify away from purely rupee denominated assets.

{.alignnone}

While MON100 typically trades at a small discount of around 5% relative to its U.S. counterpart, due to foreign exchange spreads and other fees, it is currently trading at a premium of over 15%. This is quite extreme and reflects a strong desire among Indian investors to hold foreign currency assets.

My recommendations remain the same. If you can buy foreign currency assets, especially developed world debt, both corporate and sovereign, they should do fine. If you want equity exposure, the only market I recommend right now is the U.S., as fiscal flows are keeping stock prices elevated. The same does not apply to India.

As always, for equities, I recommend cost averaging instead of lump sum investing, both in India and abroad. That said, U.S. markets generally trend upward over time, so if you really want to invest via lump sum, the U.S. is probably the better choice.

Within Indian financial assets, I would recommend sticking to money market funds, fixed deposits (FDs), and similar low risk instruments, with perhaps a small allocation to slightly riskier debt. This is where you should store your existing financial wealth.

What about those rupee denominated U.S. ETFs like MON100 that I mentioned earlier? I believe the current premium is too high to justify buying them, even considering the risk of rupee depreciation. The upside exists, but you risk losing returns if the premium compresses and the price moves back closer to NAV.

That’s all.