The mainstream media coverage of the Indian Central Government ‘budget’ has been frustrating to read and watch. It shows that the oligarchs and their cronies have complete control of the narrative presented to the public.

I want to debunk some of the ridiculous mainstream talking points regarding this budget.

1. It is Not a Budget but a Fiscal Statement

Junk economics example from The Indian Express editorial section:

The reason I put ‘budget’ in quotes in the title is that the Indian Government’s ‘budget’ is not the same as an individual’s household budget. The sole creator of the Indian Rupee is the Indian Central Government.

The term ‘budget’ makes people think that the Government has the same constraints as a household. The Government doesn’t ‘get’ the money it needs through taxes; it doesn’t need taxes to spend. Taxation and spending should be seen as two separate activities.

When you spend, you have to get the money from somewhere. For most workers, most of their income comes from wages and salaries. The same is not true for the Government; the Government creates the money which everyone else in the country uses.

If you spend more than you earn, you first draw down your savings, i.e., money you saved when you had a surplus. Once you exhaust your savings, the only solution is to go into debt. If you consistently spend more than you earn, you’ll eventually no longer be able to service your debt. At that point, no one will lend you money, and you will be bankrupt.

This is not the case with the Central Government. The Central Government creates the money you use. It cannot go bankrupt. If the Central Government’s spending is more than its revenue (which it usually is in India and most other countries), then it is injecting money into the non-Government sector. The non-Government sector (which includes you and me) is accumulating net financial wealth.

Thus, ‘fiscal statement’ is a more accurate term than ‘budget.’ The fiscal statement describes the planned revenue and expenditure of the Government. The actual expenditure can be more or less than the expenditure stated in the budget. For example, the Government’s actual expenditure on MGNREGS usually exceeds planned expenditure because of the demand-driven nature of the scheme. I’ve argued that a Job Guarantee scheme should not have a fixed budget for this very reason. For such schemes, the spending is determined by the demand for the basic job.

What happens when Government spending exceeds revenues? Under the current institutional arrangement, the Ministry of Finance issues a debt instrument, which it then sells to the RBI. The RBI is a part of the Central Government and has an obligation to purchase the debt. There is a lot of misinformation surrounding Government debt, which I will discuss further in this blog.

2. Fiscal Prudence vs. Populism is a False Dichotomy

The mainstream papers have been constantly yapping about how the Indian Government is ‘fiscally prudent’ by limiting the deficit to 4.9%. This is not ‘fiscal prudence’ but fiscal stupidity. The neoliberal claim is that if the Government enacts ‘populist’ policies like a Job Guarantee or a Universal Income, inflation would skyrocket.

The idea that increasing Government discretionary spending causes hyperinflation is complete nonsense and rooted in the false ‘Quantity Theory of Money’ (QTM). QTM states that if the Government increases ‘base money,’ inflation will occur. The QTM assumes full employment of labor and resources which is not the case in India. The fact that there is no clear relationship between money supply and inflation has been shown repeatedly in many countries.

There is nothing ‘prudent’ about leaving 30% of college graduates unemployed. It is quite the opposite of prudence; it is a waste of resources. There is nothing ‘populist’ about putting the unemployed to work under a Job Guarantee scheme. There is nothing ‘populist’ about filling hundreds of thousands of vacant Government posts . And there is nothing ‘populist’ about increasing spending on healthcare and education.

‘Fiscal Space’

The Indian Central Government’s fiscal space, i.e., the capacity to spend, should not be measured in monetary terms such as fiscal deficit or debt-to-GDP ratios. For a sovereign state, the fiscal space is the real resource space. Considering that India has high levels of labor underutilization, an increase in spending will not cause inflation.

The Government is harping on about the deficit because it thinks a low fiscal deficit will bring in foreign investment and because the markets (not people) love it. The fact that it has been doing so for the past three decades, yet unemployment remains an issue, shows that it is not working.

3. RBI giving the Government record dividends neither increases nor decreases the capacity of the Government to spend. Nor does it reduce the ability of banks to provide loans.

The RBI decided to pay a record dividend of ₹2.11 lakh crore to the Central Government for 2023–24. As stated before, this is merely accounting, like moving money from one pocket to another.

The RBI is not merely a non-profit institution; it is the institution that issues state money. The Central Government getting a ‘dividend’ from the RBI doesn’t mean anything. It neither increases nor decreases the capacity of the Government to spend. As previously stated, the Indian Central Government is not revenue-constrained. It is not constrained by taxes, nor is it constrained by ‘dividends’ from the RBI.

I saw another related argument about the RBI giving the Central Government loans reducing the money supply, which claimed that by giving ‘dividends’ to the Government, the RBI is ‘withdrawing’ money from commercial banks and reducing their ability to give loans.

Commercial banks do not work like that. They are not constrained by reserves provided by the RBI or deposits from customers.

Loans come first. A capitalist goes to the bank, gets a loan of ₹500,000, his bank account (asset) is increased by ₹500,000, but his liability also increases by the same amount since he has to pay back the amount eventually. The capitalist hires workers to build a machine and pays them ₹200,000. The workers then deposit their wages back into the bank. You can clearly see that loans create deposits, not vice-versa.

The ability to create a loan isn’t constrained by bank reserves. When the capitalist is provided the loan, the commercial bank must obtain reserves if they are insufficient. It first goes to the interbank market, where it can purchase reserves from other banks, or if the interbank market isn’t willing to lend, it can go to the central bank, which is obligated to provide the commercial bank with reserves (it is the lender of last resort for a reason).

You can see that:

a. Loans create deposits.

b. Banks are not revenue-constrained or reserve-constrained. They are constrained by people’s willingness to take loans and their creditworthiness. The willingness to take loans is determined by aggregate demand. If a capitalist sees that he can’t generate adequate profits by investing in some machinery, he won’t obtain a loan for the same.

c. Banks don’t lend the deposits; the money-multiplier concept presented in school economics textbooks is thus complete nonsense.

4. Balancing the budget is not a good thing

There is this perception in the mainstream media that the ‘best’ budget is a balanced budget, one where revenue is greater than expenditure. This is false. If aggregate demand is low and the economy is running under capacity, then fiscal deficits are a must.

You can see this with the fact that most countries across the world run consistent fiscal deficits, the exceptions being mainly developed countries with large external (usually trade) surpluses.

But even countries running external surpluses like China run a fiscal deficit. Why? Because China wants to develop. There is clearly room for development in China, just like in India. Unfortunately, neoliberal ideology is preventing India from using its full capacity.

5. Indian Government doesn’t need to borrow to fund its deficit

There has been misinformation surrounding debt. One of the talking points from the mainstream media is that the Indian Government debt has been increasing since 2016. There is nothing wrong with increasing Government debt as long as it is denominated in the currency issued by the state. Indian Government debt is mainly Rupee-denominated.

The Indian Government cannot go bankrupt in Rupees. The entire drama about Government debt is a complete farce. Indian Government debt isn’t an issue and shouldn’t be considered one.

What debt is a problem then? Private debt, of course. The rise of P2P lending, microfinance, etc., shows how desperate and financially squeezed regular Indians are. They aren’t borrowing to purchase a fancy TV but to fund their basic consumption. This is a state failure and shows that increased Government spending is required to reduce private debt.

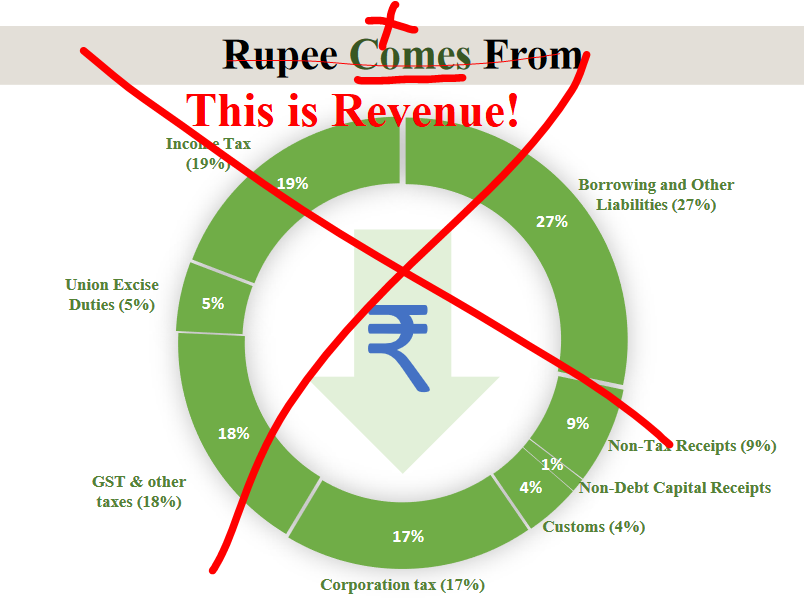

The Indian Government published a very misleading infographic showing where the Rupees ‘come from’ and ‘where it’s going.’ In reality, the Government is getting back the Rupees it previously created.

6. Indian Government doesn’t need to issue debt

The Indian Government doesn’t need to issue debt to fund its spending. It needs to issue debt to maintain its target interest rate. Why is that so? If the Government is deficit spending, there will be excess reserves in the banking system, which will bring the interbank interest rates down to near zero. This is fine, but if the Government wants to maintain a positive interest rate, it must drain the excess reserves by providing interest-yielding debt. This is what Government debt is for.

Government debt issuance doesn’t create new money; it merely swaps one asset (state money with zero interest) for another, an interest-yielding Government bond. The Government doesn’t borrow from the private sector when it issues debt for deficit spending (because of the rules, not because debt issuance is actually needed).

7. India has no ‘middle-class’

There has been much talk about this ‘budget’ being good or bad for the ‘middle class.’ However, India has no middle class with significant purchasing power. In fact, if you earn ₹25,000 a month, you are in the top 20% income percentile. This shows that the 50% income percentile (the true ‘middle class’) has really low purchasing power and isn’t consuming much because of it.

The ‘middle class’ you hear about in the media refers to the top 10-20% of the population. It is nowhere near the ‘middle’ of the income distribution.

What does this mean? The fact that most Indians aren’t part of the ‘middle class’ means the goods and services they consume remain very low. Meanwhile, the top 10-20% save a significant portion of their income, adding to their stocks of wealth. This is why wealth inequality is much worse in India than income inequality. India has no tax on wealth. Those with higher incomes can save and accumulate wealth, while those with lower incomes consume most of their income, have little to no savings, and often go into debt to meet their expenditures. This further reduces their ability to save.

What is to be done?

This year’s ‘budget’ was dogshit, and neoliberal media are trying to sugarcoat it by saying it’ll create jobs because of the Employment Linked Incentive (ELI) scheme. ELI is a fundamentally inefficient scheme. The capitalists who want to hire under ELI will be provided with much higher amounts in subsidies than the wages paid to the workers they hire. ELI is a wealth transfer scheme from the Government to the capitalists in the private sector. Much of the ELI subsidies will end up locked away in the bank accounts of the capitalists and not be used for investment or consumption, making it wasteful. For a Government that cares about fiscal deficits, they sure are willing to spend in the most inefficient ways imaginable.

Besides, given the fact that the Government has a ‘sound finance’ mindset and is unwilling to spend enough to employ the entire unemployed workforce, the budget will not change anything. The unemployment situation will remain.

Here are my suggestions:

- Stop issuing Government debt when spending. This will ensure all discussion surrounding the Government debt-to-GDP ratio is shut down.

- Don’t limit spending based on fiscal deficits; increase the spending so that the economy runs at full capacity.

- Enact a universal unconditional job guarantee with a ‘Right to Work’ constitutional amendment.

- Increase Government employee wages and fill all the vacancies in the public sector.

- Expand the public sector and increase spending on neglected sectors like railways.

- Finance state Government deficits through direct Central Government spending.

- Re-nationalize privatized assets by way of expropriation.

- Let the Rupee depreciate and instead intervene directly in the essential commodity markets.

- Bring back MSP for the entire agriculture sector and ensure that farmers aren’t forced to go into debt.

- Implement a debt jubilee for all farmers.

- Tighten controls on current and capital accounts so that the capital outflows from the mentioned policies are limited.

There are dozens more things that must be done, but these, in my opinion, are the most important.

India will be stuck with poverty, inequality, hunger, and malnutrition if it keeps going the way it is going.

That’s all.